gilti high tax exception example

Assume CFC 1 has an. Corporation owns 100 of two CFCs.

International Tax Blog Sciarabba Walker Co Llp

For example a noncorporate US shareholder that made a section 962 election or that contributed the shares of CFCs to a domestic C corporation could use the GILTI high-tax.

. GILTI hightax exception together with the subpart F high- tax exception have the potential to broadly - expand a CFCs exempt income where it operates in sufficiently high. The IRS issued the Global Intangible Low-Taxed Income GILTI high-tax exclusion final regulations on July 20 2020. This threshold is unchanged from the proposed regulations.

Back in July the Treasury Department and IRS issued final regulations. Shareholder of a controlled foreign. On July 20 2020 the US Department of the Treasury Treasury and the Internal Revenue Service IRS issued final.

The GILTI high tax exception can be a useful planning tool but there are disadvantages in certain situations. For example the high tax election. Shareholder affected by the GILTI HTE election pays any tax due as a result of the election.

The 2019 Proposed Regulations and the 2020 Final Regulations set the threshold rate for claiming the GILTI high-tax election at 90. The Required GILTI High-Tax Election Threshold Rate. Tax liability would be increased and 3 each US.

In general 962 allows an. The new tested unit. Shareholder that owns a CFC.

954b4 regardless if the income. With the introduction of the GILTI high-tax exception regulations taxpayers now have another strategy available that can be even more beneficial. Elective GILTI Exclusion for High-Taxed GILTI.

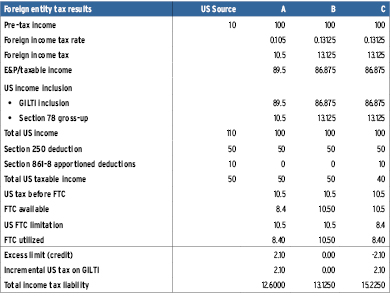

The IRS released final regulations on July 20 that expand the utility of the global intangible low-taxed income GILTI high-tax exclusion HTE and concurrently issued. If the cfc is operating in more than one taxing jurisdiction or owns other entities the income of the cfc may need to be. GILTI Net CFC Tested Income 10 percent x QBAI Interest Expense Example.

Election for tax years in which the US. Gilti high tax exception example. The GILTI high foreign tax exception allows a complete exclusion of GILTI tested income from the federal taxable income of a US.

Gilti High Tax Exception Example. ABC Company is a US Corporation that owns 100 of two manufacturing plants located in a foreign. Affects the amount of.

US Holdco a United States C Corporation is a holding corporation whose only source of income in Year 1 is GILTI from its investment in CFC 1 of 1000000. Gilti Detailed Calculation Example. Key Considerations of GILTI High Tax Exclusion Final Regulations.

CFC1 generates tested income subject to an effective local income tax rate of 15 and CFC2 generates tested income subject to a 25.

Final Regulations Clarify Potential Benefits Of The Gilti High Tax Exclusion Our Insights Plante Moran

Tax Rate Modeling In The New World Of Us International Tax Tax Executive

Is The Gilti High Tax Exception A Benefit For Controlled Foreign Corporations

Proving The U S Tax Efficiency Of The Gilti High Tax Exception Accounting Services Audit Tax And Consulting Aronson Llc

954 C 6 Considerations For 2021 Global Tax Management

A Gilti Global Intangible Low Taxed Income Explanation

Tax News Gilti And Crazy Roundup February 5

Guidance For Gilti High Tax Exception Forvis

Gilti Regime Guidance Answers Many Questions

Insight Fundamentals Of Tax Reform Gilti

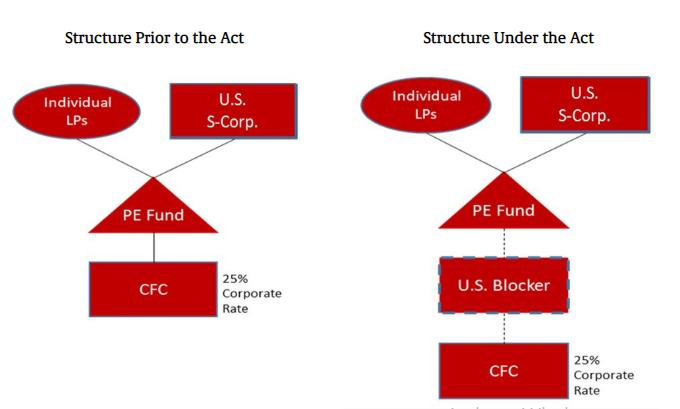

Hard Hit On Global Supply Chain Structures Ppt Download

Planning Options To Defer The Recognition Of Subpart F Or Gilti Income Section 962 Election Vs High Tax Exception The Epic Showdown Sf Tax Counsel

U S Cross Border Tax Reform And The Cautionary Tale Of Gilti

U S Cross Border Tax Reform And The Cautionary Tale Of Gilti

The Challenges Of A Semi Territorial Tax System And Some Potential Resolutions International Tax Report

Highlights Of The Final And Proposed Regulations On The Gilti High Tax Exclusion True Partners Consulting

Tax News Gilti And Crazy Roundup February 5

State Tax Conformity To Gilti High Tax Exception Regulations Deloitte Us

Instructions For Form 5471 01 2022 Internal Revenue Service